Singapore, 17 April, 2023 (Monday)

These are the research findings of the 47th round of the DBS-SKBI Singapore Index of Inflation Expectations (SInDEx) Survey at the Sim Kee Boon Institute for Financial Economics (SKBI), Singapore Management University (SMU).

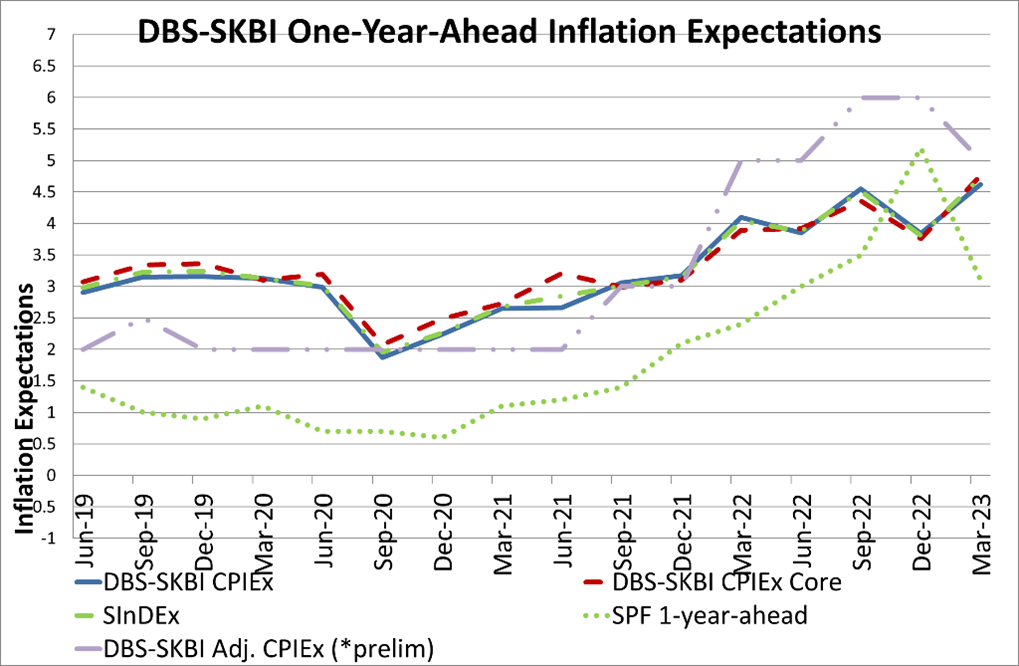

- One-year-Ahead headline inflation expectations rose to 4.6% in March 2023, from 3.8% in December 2022. This retracing of inflation expectations to September 2022 levels reflects divergent global economic signals. On one hand, global demand has been boosted with relaxation of pandemic travel restrictions, reopening of China and resolution of some supply chain disruptions. However, on the other hand, headwinds to global growth from the persistent cost-of-living crisis, tightening financial conditions, the impact of the prolonged Russia-Ukraine conflict and finally, emerging Sino-US trade tensions have dampened the global outlook. The first quarter one-year-ahead inflation expectations continue to be higher than the average one-year-ahead headline inflation expectations of 3.3% since inception between 2012-2022.

- As a comparison benchmark, data from the Monetary Authority of Singapore Survey of Professional Forecasters (MAS SPF) released in March 2023 showed that the median forecasts of CPI-All Items inflation for 2023 was 5% (for 2024, 3.1%) and MAS Core inflation was 4.1% (for 2024, 2.9%). The latest CPI data release from the Department of Statistics showed that CPI-All Items rose by 6.5% in January–February 2023, compared to the same period in 2022, with the latest February 2023 monthly inflation print coming in at 6.3% year on year. On 14 April 2023, MAS maintained the rate of appreciation of the S$NEER policy band, following five consecutive tightening moves between October 2021 - October 2022. These moves have already tempered the momentum of inflation and their impact is still working through the economy. The current appreciating path of the S$NEER policy band will continue to reduce imported inflation and help curb domestic cost pressures.

- The overall CPIEx Inflation Expectations, after adjusting for potential component-wise behavioural biases and re-combining across components, declined to 5.2% in March 2023 from 6.4% in December 2022. Inflation expectations of almost all individual components held steady or recorded declines with some divergence in expectations. From December 2022 to March 2023, one year ahead expectations of Food Inflation declined from 7% to 6%, transportation from 7% to 5%, housing and utilities from 7% to 5%, healthcare from 6% to 5%, miscellaneous components including personal care from 6% to 5%. The remaining components inflation expectations including education, recreation & culture, household durables, clothing and footwear and communications remained steady at 5% between December 2022 and March 2023 surveys.

- We also polled free response overall inflation expectations after accommodating for potential behavioural biases which declined from 6% in December 2022 to 5% in March 2023 survey.

- In the March 2023 wave, continuing from June 2022 survey, we took a more forward-looking approach to analyze the impact of global economic developments on Singapore’s economic growth and inflation.

- Overall, given the geo-political unrest and uncertainty, financial sector volatility, continuation of tightening of monetary policies by major economies, tight domestic job market and inflationary pressures Singaporean consumers felt that these developments will have a slight negative impact on Singapore’s economic growth over the next 12 months.

- Singaporean consumers also felt that over the next 12 months, they will have to spend slightly higher amounts owing mainly to price increases.

- In March 2023, we polled consumers on how they feel the overall inflation scenario would unfold in the next 12 months. Around 50% (compared to 41% in December 2022) of those surveyed expect inflation to decline while 41% (compared to 45% in December 2022) felt that it will increase.

- The main reasons for for these shifts in consumers’ expectations are central banks in major economies raising interest rates (41%), second highest being slowdown in global growth (35%). Resolution of pandemic-induced supply chain disruptions are also expected to relieve price pressures. The main reasons cited by respondents for increase in inflation over the next 12 months were also central banks in major economies raising interest rates (36%), followed by higher demand due to relaxation of pandemic restrictions (27%) and geopolitical uncertainties due to the Ukraine-Russia conflict (23%). Lingering supply chain disruptions account for about 11% of those who thought prices will go up.

- In the March 2023 survey, we found current economic conditions having a moderate negative impact on one-year-ahead and five-year-ahead overall inflation expectations. This slight negative impact is also polled across components like Food, transportation, housing and utilities, healthcare, clothing & footwear, household durables & services, but there was no discernable impact on education, recreation & culture, communications, and miscellaneous items including personal effects.

- There were however some divergences among respondents regarding the impact on inflation expectations for certain components including food, transportation, housing & utilities, healthcare, clothing & footwear, household durables & services, and overall one-year and five-year ahead inflation expectations where we find a distinct bimodal distributions, which means there are two large groups who disagree whether the impact would be positive or negative reflecting the global uncertainty.

- Following the academic work by Alberto Cavallo of Harvard Business School (2020) and the UK Office of National Statistics (ONS), respondents were asked if there were any substantive changes to their consumption basket. In the March 2023 survey, results indicate that respondents expect the consumptions baskets to remain unchanged over the next twelve months signaling continued normalisation of post-pandemic relative consumption and price patterns across the board.

- Excluding expectations of accommodation and private transportation inflation, the One-year-Ahead CPIEx core inflation expectations in March 2023 survey elevated to 4.8 % from 3.8% in December 2022, in line with overall inflation expectations.

- For a subgroup of the population who owns their accommodation and uses public transport, the One-year-Ahead CPIEx core inflation expectations elevated to 4.7 % in March 2023 from 3.6% in December 2022, corroborating the increase in core inflation expectations. This sub-sample measurement is potentially more representative than the full sample measurement, due to high home ownership and public transport ridership in Singapore.

- However, unlike the fixed response which might be amenable to behavioural biases, core CPIEx Inflation Expectations (excluding accommodation and private road transportation expenses), after adjusting for potential component-wise behavioural biases and re-combining across components, declined to 5.3% in March 2023 from 6.1% in December 2022 survey. The free response core CPIEx Inflation Expectations also declined to 5% in March 2023 from 6% in December 2022 poll.

- The One-year-Ahead composite index SInDEx1 that puts less weight on more volatile components like accommodation, private road transport, food and energy related expenses polled at 4.7% in March 2023 elevated from 3.8 % in December 2022. It continues to be higher than the first quarter average of 3.4% since the survey’s inception from 2012 till 2022.

- In addition, in March 2023, around 9.8% of the Singaporeans polled expect a more than 5.0% reduction in salary in the next 12 months. This is a slightly less compared to 10.8% in December 2022. The median salary increment expectation remained unchanged compared to September 2022 survey at an increase by 1.0%-5.0%.

Figure 1: One-year-Ahead inflation expectations: The chart shows the quarterly DBS-SKBI CPIEx (CPI-All Item) and DBS-SKBI CPIEx Core (Excluding accommodation and private road transportation components) One-Year-Ahead Inflation Expectations polled in the quarterly online Singapore Index of Inflation Expectations (SInDEx) Survey conducted March 14-21, 2023. [Source: SKBI, SMU, MAS, Department of Statistics]

DBS Chief Economist and Managing Director of Group Research, Dr. Taimur Baig, commented, “Overall inflation may have peaked worldwide, but for the average individual, cost of living remains elevated, with pressures coming from rent, services, and operations. Inflation expectations are also somewhat volatile, which is understandable given the adjustments needed after a prolonged period of low and steady inflation pre-pandemic. We expect the lagged impact of several bouts of MAS policy tightening to eventually stabilise inflation expectations in Singapore.”

SMU Assistant Professor of Finance and Founding Principal Investigator of the Quarterly DBS-SKBI SInDEx Project, Aurobindo Ghosh, highlighted, “The International Monetary Fund (IMF) in their semiannual World Economic Outlook released in April 2023 highlights a ‘broad-based sharper-than-expected slowdown,’ with the cost-of-living crisis, geopolitical tensions like the Russia-Ukraine conflict, tightening financial conditions including collapse of the mid-size Silicon Valley Bank and vestiges of the global pandemic weighing down on the economic outlook including slower global growth. Domestically, Singapore consumers have been facing elevated price pressures emanating from a tighter labor market, and other pass-through costs including rental and energy. However, a discernable slowdown in global growth particularly in advanced economies despite the reopening in China which is also swaying the opinions of consumers who seem suggest medium term inflation expectations are still elevated.”

“Survey based inflation expectations measures are well-known to suffer from certain behavioural biases like the ‘anchoring bias,’ where the questionnaire design or positioning of options might influence opinions. DBS-SKBI SInDEx Inflation Expectations survey accommodated for some of the behavioural biases by using multiple choice based and free response options.

Accommodating for wider choice set, it seems that the behaviourally adjusted free response seem to correspond to the choice-based answers to reduce the ‘cognitive dissonance.’ Overall, the behaviourally adjusted responses suggest that the level of uncertainty might be reducing, and respondents provide a slightly elevated one-year ahead inflation expectations. However, opinions seem to be divided fairly even across the population about the direction of inflation outcome. This dichotomy, with one group expecting inflation to pare down while other expecting inflation rate to rise, can be reconciled by the duration it takes for tightening monetary policy reduce prices in a globalised marketplace, particularly for a small open economy like Singapore, which might see short run increases of prices followed by longer run declines,” Assistant Prof Ghosh observed.

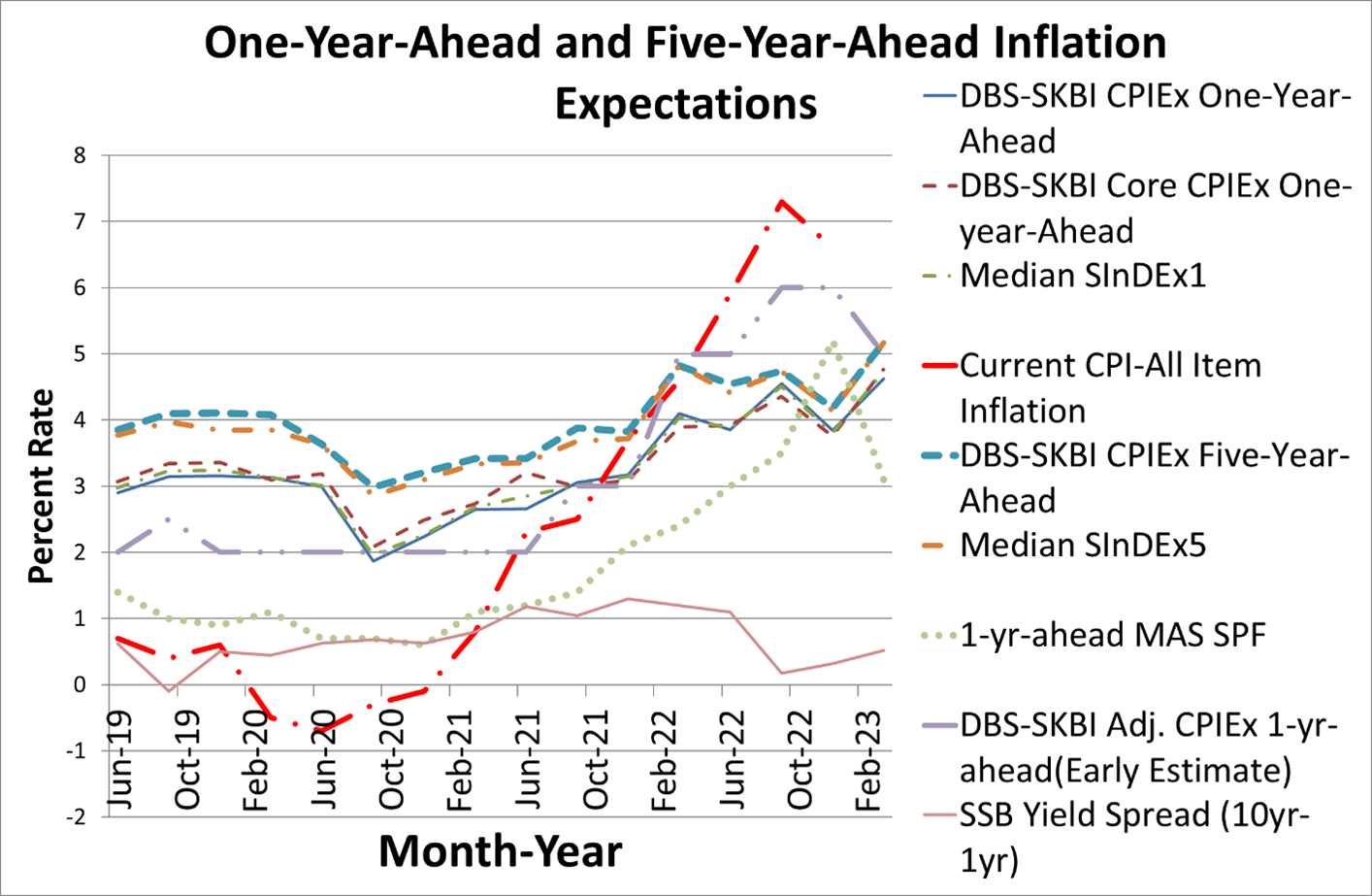

For the longer horizon, the Five-year-Ahead CPIEx inflation expectations elevated to 5.2% in March 2023 from 4.2% in the December 2022 survey. The current polled number continues to be higher than the first quarter average of 4.2% since the survey’s inception in 2012.

The Five-year-Ahead CPIEx core inflation expectations (excluding accommodation and private road transportation related costs) also increased to 5.2% in March 2023 from 4.1% in December 2022. Overall, the composite Five-year-Ahead SInDEx5 also increased to 5.2% in March 2023 from 4.1% in December 2022. In comparison, the first quarter average value (since the survey’s inception in 2012 till 2022) of the composite Five-year-Ahead SInDEx5 is 4.0%.

After adjusting for potential behavioural biases, the free response Five-Year-Ahead Headline Inflation Expectations declined to 5% in March 2023 from 6% in December 2022, although free response Core Five-Year-Ahead Inflation Expectations remained unchanged at 6%.

“The unadjusted long term five-year-ahead inflation expectations seem to be treading closely with the medium term inflation expectations. However, when evaluating the longer term inflation expectations, adjusting for behavioural biases, the longer term inflation expectations seem to be moderating. This signals there is some degree of anchoring of long-term inflation expectations despite the high degree of global geopolitical uncertainty and global economic headwinds. Policymakers around the world seem to be treading more cautiously on curbing inflation to avoid a ‘hard landing’ with policy normalization amidst global headwinds for economic growth,” Assistant Prof Ghosh commented.

Figure 2: Five-year-Ahead-Inflation Expectations in Singapore: The chart shows the quarterly DBS-SKBI CPIEx (CPI-All Item), DBS-SKBI CPIEx Core (excluding accommodation and private road transportation components), SInDEx (Composite index with lower weights on volatile components like food, energy, accommodation and private road transportation) One-Year and Five-Year-Ahead Inflation Expectations polled online quarterly for the Singapore Index of Inflation Expectations (SInDex) Survey conducted March 14-21, 2023. The chart shows a preliminary estimate of Behaviourally Adjusted One-year-Ahead overall DBS-SKBI Adjusted CPIEx. As comparison benchmarks, the chart provides the most recent quarterly CPI-All Item Inflation, MAS Survey of Professional Forecasters median One-year-Ahead CPI-All Item inflation forecasts and the yield spread of 10-year and 1-year Singapore Savings Bonds (SSB). [Source:SKBI, SMU, MAS, Department of Statistics]

Methodology

DBS-SKBI SInDEx survey yields CPIEx Inflation Expectations (estimating headline inflation expectations) and related indices are products of the online quarterly survey of around 500 randomly selected individuals representing a cross section of Singaporean households. The survey is led by Principal Investigator Dr. Aurobindo Ghosh, Assistant Professor of Finance (Education) at Lee Kong Chian School of Business, SMU. The online survey, powered by Agility Research and Strategy, helps researchers understand the behavior and sentiments of decision makers in Singaporean households. DBS Group Research is a co-sponsor and research partner with the Sim Kee Boon Institute for Financial Economics (SKBI) at SMU.

The quarterly DBS-SKBI SInDEx survey has also yielded two composite indices, SInDEx1 and SInDEx5. SInDEx1 and SInDEx5 measure the One-year inflation expectations and the Five-year inflation expectations, respectively. The sampling was done using a quota sample over gender, age and residency status to ensure representativeness of the sample. Employees in some sectors like journalism and marketing were excluded as that might have an effect on their responses to questions on consumption behavior and expectations.

The DBS-SKBI SInDEx survey was augmented in June 2018, based on a joint research study conducted by SMU researchers in collaboration with MAS and the Behavioral Insights Team, where respondents were polled on their perceptions of components of the Consumers Price Index (CPI) and adjusted for possible behavioral biases prevalent in online surveys.

Based on the recommendations of the joint study, since March 2019 the research team has polled the One-year-Ahead inflation expectations of all of the major components of CPI-All Items inflation. For March 2022 survey, DBS-SKBI CPIEx headline and core inflation expectations indices increased compared to December 2022. However, the behaviorally adjusted component-wise and recombined inflation expectations had differential responses, causing the overall behaviorally adjusted indices to decline slightly. In free response answers, compared to December 2022 survey, respondents in the March 2023 survey polled One-year Ahead Headline rate declined. Following suit, one-year ahead core inflation expectations, adjusted for behavioral biases, declined slightly. However, as a positive sign of anchoring, free response Five-year Ahead headline has declined slightly while the five-year-ahead core inflation was unchanged.

We introduced a new ratio in the June 2020 survey, on the life versus livelihood debate as an aftermath of the Covid 19 pandemic - the ratio of respondents who feels livelihood should be prioritised over life vis-à-vis those who feel the other way. This ratio remained unchanged at 3 in March 2023, slightly lower than December 2022. For every respondent who prioritised life over livelihood, there were about 3 who prioritised livelihood over life, signaling a level of stabilization though there are still divergent groups.

DBS-SKBI press release_17Apr2023_final.pdf

Originally published at https://news.smu.edu.sg/news/2023/04/17/inflation-expectations-more-mixed-weakening-global-economic-conditions

Back to Research@SMU May 2023 Issue

Want to see more of SMU Research?

Sign up for Research@SMU e-newslettter to know more about our research and research-related events!

If you would like to remove yourself from all our mailing list, please visit https://eservices.smu.edu.sg/internet/DNC/Default.aspx